Can You Get a Mortgage for a Mobile Home

A mortgage loan or simply mortgage () is a loan used either past purchasers of real belongings to raise funds to buy real estate, or by existing holding owners to raise funds for any purpose while putting a lien on the belongings existence mortgaged. The loan is "secured" on the borrower's property through a process known every bit mortgage origination. This ways that a legal mechanism is put into place which allows the lender to take possession and sell the secured property ("foreclosure" or "repossession") to pay off the loan in the issue the borrower defaults on the loan or otherwise fails to abide by its terms. The discussion mortgage is derived from a Police force French term used in Uk in the Centre Ages significant "decease pledge" and refers to the pledge ending (dying) when either the obligation is fulfilled or the property is taken through foreclosure.[ane] A mortgage can besides be described as "a borrower giving consideration in the form of a collateral for a benefit (loan)".

Mortgage borrowers can be individuals mortgaging their home or they can be businesses mortgaging commercial property (for example, their own business organisation premises, residential property let to tenants, or an investment portfolio). The lender will typically exist a fiscal institution, such every bit a bank, credit matrimony or building guild, depending on the country concerned, and the loan arrangements can be made either directly or indirectly through intermediaries. Features of mortgage loans such as the size of the loan, maturity of the loan, interest rate, method of paying off the loan, and other characteristics tin can vary considerably. The lender's rights over the secured belongings accept priority over the borrower'south other creditors, which means that if the borrower becomes bankrupt or insolvent, the other creditors volition only be repaid the debts owed to them from a sale of the secured property if the mortgage lender is repaid in full commencement.

In many jurisdictions, it is normal for home purchases to be funded by a mortgage loan. Few individuals accept enough savings or liquid funds to enable them to buy property outright. In countries where the demand for habitation ownership is highest, strong domestic markets for mortgages accept developed. Mortgages can either be funded through the banking sector (that is, through short-term deposits) or through the majuscule markets through a procedure called "securitization", which converts pools of mortgages into fungible bonds that can exist sold to investors in small denominations.

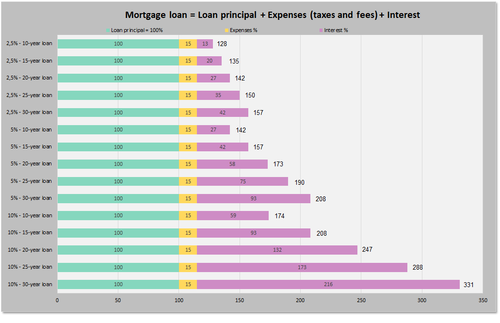

Mortgage Loan. Total Payment (3 Fixed Involvement Rates & 2 Loan Term) = Loan Principal + Expenses (Taxes & fees) + Total involvement to exist paid.

The terminal cost will exist exactly the aforementioned:

* when the involvement charge per unit is 2.5% and the term is xxx years than when the interest rate is 5% and the term is 15 years * when the interest rate is v% and the term is 30 years than when the interest rate is x% and the term is 15 years

Mortgage loan nuts

Basic concepts and legal regulation

Co-ordinate to Anglo-American property law, a mortgage occurs when an owner (normally of a fee unproblematic involvement in realty) pledges his or her interest (right to the property) as security or collateral for a loan. Therefore, a mortgage is an encumbrance (limitation) on the correct to the property merely every bit an easement would be, but because about mortgages occur as a condition for new loan coin, the word mortgage has become the generic term for a loan secured by such existent property. As with other types of loans, mortgages have an interest rate and are scheduled to amortize over a set flow of time, typically 30 years. All types of real property tin be, and commonly are, secured with a mortgage and acquit an involvement rate that is supposed to reflect the lender'south hazard.

Mortgage lending is the master machinery used in many countries to finance private buying of residential and commercial belongings (see commercial mortgages). Although the terminology and precise forms will differ from country to country, the basic components tend to exist similar:

- Property: the physical residence being financed. The verbal class of ownership volition vary from country to country and may restrict the types of lending that are possible.

- Mortgage: the security interest of the lender in the property, which may entail restrictions on the use or disposal of the property. Restrictions may include requirements to purchase habitation insurance and mortgage insurance, or pay off outstanding debt earlier selling the property.

- Borrower: the person borrowing who either has or is creating an buying interest in the property.

- Lender: any lender, but usually a banking company or other financial institution. (In some countries, particularly the United states, Lenders may too exist investors who own an interest in the mortgage through a mortgage-backed security. In such a situation, the initial lender is known every bit the mortgage originator, which then packages and sells the loan to investors. The payments from the borrower are thereafter nerveless by a loan servicer.[2])

- Main: the original size of the loan, which may or may not include certain other costs; as any principal is repaid, the principal volition go downward in size.

- Interest: a financial charge for use of the lender'due south money.

- Foreclosure or repossession: the possibility that the lender has to forestall, reclaim or seize the property under sure circumstances is essential to a mortgage loan; without this aspect, the loan is arguably no different from any other type of loan.

- Completion: legal completion of the mortgage deed, and hence the start of the mortgage.

- Redemption: final repayment of the corporeality outstanding, which may be a "natural redemption" at the cease of the scheduled term or a lump sum redemption, typically when the borrower decides to sell the holding. A airtight mortgage business relationship is said to be "redeemed".

Many other specific characteristics are common to many markets, just the higher up are the essential features. Governments usually regulate many aspects of mortgage lending, either directly (through legal requirements, for example) or indirectly (through regulation of the participants or the financial markets, such as the banking manufacture), and oft through state intervention (direct lending by the government, direct lending by land-endemic banks, or sponsorship of various entities). Other aspects that define a specific mortgage market place may be regional, historical, or driven by specific characteristics of the legal or financial system.

Mortgage loans are generally structured equally long-term loans, the periodic payments for which are similar to an annuity and calculated according to the time value of money formulae. The near basic organisation would require a fixed monthly payment over a period of ten to thirty years, depending on local conditions. Over this period the principal component of the loan (the original loan) would be slowly paid down through amortization. In practise, many variants are possible and mutual worldwide and within each country.

Lenders provide funds against property to earn involvement income, and by and large borrow these funds themselves (for instance, by taking deposits or issuing bonds). The price at which the lenders borrow money, therefore, affects the cost of borrowing. Lenders may besides, in many countries, sell the mortgage loan to other parties who are interested in receiving the stream of greenbacks payments from the borrower, often in the course of a security (by means of a securitization).

Mortgage lending will too take into account the (perceived) riskiness of the mortgage loan, that is, the likelihood that the funds volition exist repaid (commonly considered a role of the creditworthiness of the borrower); that if they are not repaid, the lender volition be able to foreclose on the real manor assets; and the financial, interest rate risk and fourth dimension delays that may be involved in certain circumstances.

Mortgage underwriting

During the mortgage loan approving process, a mortgage loan underwriter verifies the financial information that the applicant has provided equally to income, employment, credit history and the value of the home being purchased via an appraisal.[3] An appraisal may be ordered. The underwriting process may take a few days to a few weeks. Sometimes the underwriting process takes and so long that the provided financial statements need to be resubmitted and then they are current.[4] Information technology is advisable to maintain the same employment and non to use or open new credit during the underwriting process. Whatsoever changes fabricated in the applicant's credit, employment, or financial information could result in the loan being denied.

Mortgage loan types

At that place are many types of mortgages used worldwide, simply several factors broadly ascertain the characteristics of the mortgage. All of these may exist subject to local regulation and legal requirements.

- Interest: Interest may exist fixed for the life of the loan or variable, and change at sure pre-defined periods; the interest rate can besides, of course, be higher or lower.

- Term: Mortgage loans generally have a maximum term, that is, the number of years after which an amortizing loan will be repaid. Some mortgage loans may accept no amortization, or require total repayment of any remaining balance at a certain engagement, or fifty-fifty negative amortization.

- Payment amount and frequency: The amount paid per period and the frequency of payments; in some cases, the corporeality paid per period may alter or the borrower may have the pick to increase or decrease the corporeality paid.

- Prepayment: Some types of mortgages may limit or restrict prepayment of all or a portion of the loan, or require payment of a penalty to the lender for prepayment.

The two basic types of amortized loans are the fixed rate mortgage (FRM) and adjustable-rate mortgage (ARM) (also known as a floating rate or variable charge per unit mortgage). In some countries, such as the United States, stock-still rate mortgages are the norm, simply floating charge per unit mortgages are relatively common. Combinations of fixed and floating rate mortgages are besides common, whereby a mortgage loan will accept a fixed rate for some period, for case the first v years, and vary after the stop of that menses.

- In a stock-still-rate mortgage, the interest charge per unit, remains stock-still for the life (or term) of the loan. In the case of an annuity repayment scheme, the periodic payment remains the same amount throughout the loan. In the instance of linear payback, the periodic payment volition gradually decrease.

- In an adjustable-charge per unit mortgage, the involvement charge per unit is generally fixed for a period of fourth dimension, after which it will periodically (for example, annually or monthly) adjust upward or downwardly to some market index. Adjustable rates transfer role of the interest rate risk from the lender to the borrower and thus are widely used where fixed rate funding is difficult to obtain or prohibitively expensive. Since the risk is transferred to the borrower, the initial interest charge per unit may be, for example, 0.five% to ii% lower than the boilerplate 30-year stock-still rate; the size of the price differential will exist related to debt marketplace atmospheric condition, including the yield bend.

The charge to the borrower depends upon the credit take a chance in addition to the interest rate risk. The mortgage origination and underwriting process involves checking credit scores, debt-to-income, downpayments, avails, and assessing belongings value. Jumbo mortgages and subprime lending are not supported by government guarantees and face up higher interest rates. Other innovations described below tin affect the rates likewise.

Loan to value and downwards payments

Upon making a mortgage loan for the buy of a holding, lenders usually require that the borrower make a downwards payment; that is, contribute a portion of the price of the belongings. This downward payment may be expressed as a portion of the value of the holding (see below for a definition of this term). The loan to value ratio (or LTV) is the size of the loan against the value of the property. Therefore, a mortgage loan in which the purchaser has made a down payment of 20% has a loan to value ratio of lxxx%. For loans made against properties that the borrower already owns, the loan to value ratio volition be imputed against the estimated value of the property.

The loan to value ratio is considered an important indicator of the riskiness of a mortgage loan: the college the LTV, the higher the chance that the value of the belongings (in case of foreclosure) volition be insufficient to cover the remaining principal of the loan.

Value: appraised, estimated, and actual

Since the value of the property is an important cistron in understanding the hazard of the loan, determining the value is a central factor in mortgage lending. The value may be determined in various ways, simply the nearly common are:

- Actual or transaction value: this is ordinarily taken to be the buy price of the property. If the property is not existence purchased at the time of borrowing, this data may not be bachelor.

- Appraised or surveyed value: in most jurisdictions, some grade of appraisement of the value by a licensed professional is common. There is often a requirement for the lender to obtain an official appraisal.

- Estimated value: lenders or other parties may employ their ain internal estimates, particularly in jurisdictions where no official appraisal procedure exists, but also in some other circumstances.

Payment and debt ratios

In most countries, a number of more or less standard measures of creditworthiness may be used. Common measures include payment to income (mortgage payments as a percentage of gross or net income); debt to income (all debt payments, including mortgage payments, every bit a pct of income); and various internet worth measures. In many countries, credit scores are used in lieu of or to supplement these measures. In that location will also be requirements for documentation of the creditworthiness, such every bit income tax returns, pay stubs, etc. the specifics will vary from location to location. Income revenue enhancement incentives usually tin can be applied in forms of tax refunds or tax deduction schemes. The first implies that income tax paid past individual taxpayers volition exist refunded to the extent of involvement on mortgage loans taken to acquire residential property. Income tax deduction implies lowering tax liability to the extent of involvement rate paid for the mortgage loan.

Some lenders may as well require a potential borrower have 1 or more months of "reserve avails" bachelor. In other words, the borrower may be required to show the availability of enough assets to pay for the housing costs (including mortgage, taxes, etc.) for a period of fourth dimension in the upshot of the chore loss or other loss of income.

Many countries have lower requirements for certain borrowers, or "no-doc" / "low-dr." lending standards that may be acceptable nether certain circumstances.

Standard or conforming mortgages

Many countries have a notion of standard or conforming mortgages that define a perceived acceptable level of risk, which may be formal or informal, and may be reinforced past laws, government intervention, or market exercise. For example, a standard mortgage may be considered to exist one with no more than than seventy–80% LTV and no more one-third of gross income going to mortgage debt.

A standard or conforming mortgage is a key concept as information technology often defines whether or not the mortgage can be hands sold or securitized, or, if non-standard, may impact the price at which it may be sold. In the U.s.a., a befitting mortgage is one which meets the established rules and procedures of the two major government-sponsored entities in the housing finance market place (including some legal requirements). In contrast, lenders who decide to make nonconforming loans are exercising a college risk tolerance and practise then knowing that they confront more challenge in reselling the loan. Many countries have similar concepts or agencies that define what are "standard" mortgages. Regulated lenders (such as banks) may be subject field to limits or higher-risk weightings for non-standard mortgages. For case, banks and mortgage brokerages in Canada face up restrictions on lending more than than eighty% of the property value; beyond this level, mortgage insurance is generally required.[five]

Foreign currency mortgage

In some countries with currencies that tend to depreciate, foreign currency mortgages are mutual, enabling lenders to lend in a stable foreign currency, whilst the borrower takes on the currency risk that the currency will depreciate and they volition therefore need to convert higher amounts of the domestic currency to repay the loan.

Repaying the mortgage

Mortgage Loan. Total Payment = Loan Master + Expenses (Taxes & fees) + Total interests. Fixed Interest Rates & Loan Term

In add-on to the two standard means of setting the price of a mortgage loan (fixed at a fix interest rate for the term, or variable relative to market interest rates), there are variations in how that cost is paid, and how the loan itself is repaid. Repayment depends on locality, tax laws and prevailing civilisation. There are also various mortgage repayment structures to suit different types of borrower.

Principal and interest

The nigh common manner to repay a secured mortgage loan is to make regular payments toward the principal and interest over a prepare term.[ commendation needed ] This is commonly referred to as (self) amortization in the U.S. and as a repayment mortgage in the Britain. A mortgage is a form of annuity (from the perspective of the lender), and the calculation of the periodic payments is based on the time value of money formulas. Certain details may be specific to different locations: interest may be calculated on the basis of a 360-day twelvemonth, for example; interest may be compounded daily, yearly, or semi-annually; prepayment penalties may utilize; and other factors. In that location may exist legal restrictions on sure matters, and consumer protection laws may specify or prohibit sure practices.

Depending on the size of the loan and the prevailing practice in the country the term may exist brusque (10 years) or long (l years plus). In the Uk and U.South., 25 to 30 years is the usual maximum term (although shorter periods, such equally 15-yr mortgage loans, are common). Mortgage payments, which are typically fabricated monthly, comprise a repayment of the principal and an involvement element. The amount going toward the principal in each payment varies throughout the term of the mortgage. In the early on years the repayments are by and large interest. Towards the end of the mortgage, payments are mostly for principal. In this way, the payment corporeality determined at offset is calculated to ensure the loan is repaid at a specified date in the hereafter. This gives borrowers assurance that past maintaining repayment the loan volition exist cleared at a specified engagement if the interest rate does not change. Some lenders and 3rd parties offering a bi-weekly mortgage payment program designed to accelerate the payoff of the loan. Similarly, a mortgage can be concluded before its scheduled cease by paying some or all of the remainder prematurely, chosen curtailment.[6]

An amortization schedule is typically worked out taking the principal left at the end of each month, multiplying past the monthly charge per unit then subtracting the monthly payment. This is typically generated by an amortization estimator using the following formula:

where:

- is the periodic acquittal payment

- is the principal amount borrowed

- is the rate of interest expressed as a fraction; for a monthly payment, take the (Almanac Charge per unit)/12

- is the number of payments; for monthly payments over 30 years, 12 months 10 xxx years = 360 payments.

Interest simply

The master culling to a principal and interest mortgage is an interest-only mortgage, where the principal is not repaid throughout the term. This type of mortgage is common in the UK, specially when associated with a regular investment plan. With this arrangement regular contributions are made to a separate investment programme designed to build up a lump sum to repay the mortgage at maturity. This type of arrangement is called an investment-backed mortgage or is often related to the type of plan used: endowment mortgage if an endowment policy is used, similarly a personal equity plan (PEP) mortgage, Individual Savings Account (ISA) mortgage or pension mortgage. Historically, investment-backed mortgages offered various tax advantages over repayment mortgages, although this is no longer the example in the Britain. Investment-backed mortgages are seen as higher run a risk as they are dependent on the investment making sufficient return to articulate the debt.

Until recently[ when? ] it was not uncommon for involvement only mortgages to be bundled without a repayment vehicle, with the borrower gambling that the belongings market will rise sufficiently for the loan to be repaid by trading downwards at retirement (or when rent on the belongings and aggrandizement combine to surpass the interest charge per unit)[ citation needed ].

Interest-simply lifetime mortgage

Recent Financial Services Authorisation guidelines to UK lenders regarding interest-only mortgages has tightened the criteria on new lending on an interest-only ground. The problem for many people has been the fact that no repayment vehicle had been implemented, or the vehicle itself (e.g. endowment/ISA policy) performed poorly and therefore insufficient funds were available to repay balance at the end of the term.

Moving forward, the FSA under the Mortgage Market place Review (MMR) take stated in that location must be strict criteria on the repayment vehicle being used. Every bit such the likes of Nationwide and other lenders have pulled out of the interest-only market.

A resurgence in the equity release market has been the introduction of involvement-only lifetime mortgages. Where an interest-just mortgage has a fixed term, an interest-merely lifetime mortgage volition keep for the rest of the mortgagors life. These schemes have proved of interest to people who practise like the roll-upwardly event (compounding) of interest on traditional equity release schemes. They have also proved beneficial to people who had an involvement-only mortgage with no repayment vehicle and at present demand to settle the loan. These people can at present effectively remortgage onto an interest-but lifetime mortgage to maintain continuity.

Interest-only lifetime mortgage schemes are currently offered past ii lenders – Stonehaven and more2life. They piece of work by having the options of paying the interest on a monthly footing. Past paying off the interest means the balance will remain level for the rest of their life. This market is set to increase as more retirees crave finance in retirement.

Contrary mortgages

For older borrowers (typically in retirement), it may be possible to arrange a mortgage where neither the principal nor interest is repaid. The interest is rolled upwardly with the primary, increasing the debt each twelvemonth.

These arrangements are variously called reverse mortgages, lifetime mortgages or equity release mortgages (referring to home equity), depending on the land. The loans are typically non repaid until the borrowers are deceased, hence the age restriction.

Through the Federal Housing Administration, the U.S. government insures opposite mortgages via a program called the HECM (Home Equity Conversion Mortgage). Dissimilar standard mortgages (where the entire loan amount is typically disbursed at the time of loan closing) the HECM program allows the homeowner to receive funds in a variety of means: equally a one time lump sum payment; as a monthly tenure payment which continues until the borrower dies or moves out of the house permanently; as a monthly payment over a defined catamenia of time; or equally a credit line.[seven]

For further details, see disinterestedness release.

Interest and fractional primary

In the U.South. a partial amortization or airship loan is one where the amount of monthly payments due are calculated (amortized) over a sure term, merely the outstanding residuum on the main is due at some point short of that term. In the UK, a partial repayment mortgage is quite common, specially where the original mortgage was investment-backed.

Variations

Graduated payment mortgage loans have increasing costs over fourth dimension and are geared to young borrowers who await wage increases over fourth dimension. Balloon payment mortgages have only partial amortization, meaning that amount of monthly payments due are calculated (amortized) over a certain term, just the outstanding principal residual is due at some indicate short of that term, and at the finish of the term a balloon payment is due. When interest rates are high relative to the rate on an existing seller's loan, the heir-apparent tin consider assuming the seller's mortgage.[8] A wraparound mortgage is a form of seller financing that tin make information technology easier for a seller to sell a property. A biweekly mortgage has payments made every two weeks instead of monthly.

Budget loans include taxes and insurance in the mortgage payment;[ix] package loans add the costs of effects and other personal property to the mortgage. Buydown mortgages allow the seller or lender to pay something like to points to reduce interest rate and encourage buyers.[10] Homeowners can as well take out disinterestedness loans in which they receive cash for a mortgage debt on their firm. Shared appreciation mortgages are a course of equity release. In the U.s.a., strange nationals due to their unique situation confront Strange National mortgage conditions.

Flexible mortgages allow for more freedom by the borrower to skip payments or prepay. Starting time mortgages allow deposits to exist counted against the mortgage loan. In the UK at that place is besides the endowment mortgage where the borrowers pay interest while the main is paid with a life insurance policy.

Commercial mortgages typically have different interest rates, risks, and contracts than personal loans. Participation mortgages allow multiple investors to share in a loan. Builders may take out blanket loans which embrace several properties at in one case. Bridge loans may be used as temporary financing awaiting a longer-term loan. Hard money loans provide financing in substitution for the mortgaging of real manor collateral.

Foreclosure and non-recourse lending

In most jurisdictions, a lender may forestall the mortgaged belongings if certain conditions occur – principally, non-payment of the mortgage loan. Subject to local legal requirements, the property may then exist sold. Whatsoever amounts received from the auction (net of costs) are applied to the original debt. In some jurisdictions, mortgage loans are non-recourse loans: if the funds recouped from auction of the mortgaged belongings are bereft to embrace the outstanding debt, the lender may non have recourse to the borrower after foreclosure. In other jurisdictions, the borrower remains responsible for any remaining debt.

In virtually all jurisdictions, specific procedures for foreclosure and sale of the mortgaged property apply, and may exist tightly regulated past the relevant government. There are strict or judicial foreclosures and non-judicial foreclosures, also known as power of sale foreclosures. In some jurisdictions, foreclosure and sale can occur quite rapidly, while in others, foreclosure may accept many months or even years. In many countries, the ability of lenders to forbid is extremely limited, and mortgage market development has been notably slower.

National differences

A study issued by the UN Economic Commission for Europe compared German, US, and Danish mortgage systems. The High german Bausparkassen have reported nominal interest rates of approximately 6 per cent per annum in the terminal 40 years (as of 2004). German Bausparkassen (savings and loans associations) are not identical with banks that give mortgages. In addition, they charge administration and service fees (about 1.v per cent of the loan amount). However, in the United states, the boilerplate involvement rates for fixed-rate mortgages in the housing market place started in the tens and twenties in the 1980s and have (as of 2004) reached nigh 6 per cent per annum. However, gross borrowing costs are substantially higher than the nominal interest charge per unit and amounted for the last xxx years to 10.46 per cent. In Denmark, similar to the U.s. mortgage market, involvement rates take fallen to 6 per cent per annum. A run a risk and administration fee amounts to 0.5 per cent of the outstanding debt. In addition, an acquisition fee is charged which amounts to 1 per cent of the main.[xi]

United states

The mortgage manufacture of the Us is a major fiscal sector. The federal government created several programs, or government sponsored entities, to foster mortgage lending, structure and encourage home ownership. These programs include the Regime National Mortgage Association (known as Ginnie Mae), the Federal National Mortgage Association (known as Fannie Mae) and the Federal Home Loan Mortgage Corporation (known as Freddie Mac).

The US mortgage sector has been the center of major financial crises over the concluding century. Unsound lending practices resulted in the National Mortgage Crisis of the 1930s, the savings and loan crisis of the 1980s and 1990s and the subprime mortgage crisis of 2007 which led to the 2010 foreclosure crisis.

In the United States, the mortgage loan involves two separate documents: the mortgage note (a promissory note) and the security interest evidenced by the "mortgage" certificate; generally, the two are assigned together, but if they are split traditionally the holder of the note and not the mortgage has the right to foreclose.[12] For example, Fannie Mae promulgates a standard form contract Multistate Fixed-Rate Notation 3200[13] and as well divide security instrument mortgage forms which vary by country.[14]

History in the United States

The idea of purchasing land is a relatively new idea. The idea of credit being used to purchase land originated with the British colonies in the futurity United states. The colonists did not give ethnic people already living in America any money for the land they took from them. This was not the only shocking divergence between pre-colonized America and post-colonized America. There were huge environmental and biological changes, which led to social, economic, and political changes. There was new types of violence and diseases brought to America. The colonists traded with "wampum,"[xv] which was a string of shell beads in dissimilar colors and shells. White ones were chosen wompi, black ones were called sucka uhock. Round clams were worth twice as much as the white wompi shells. They were around one-eighth of an inch in diameter and one-quarter inch in length. Colonists attempted to trade with indigenous people for skins by growing corn. Just corn could not get the colonists the best skins, such equally beaver skins. The shells were chosen to be used as money because of the symbolic meaning they held for the tribes. Indigenous people believed the shells came from a blazon of God.[15] The shells could fifty-fifty be talked into to go along words and stories. On the colonists' side, there was also a significance that the indigenous people did non understand. Colonists from England actively pursued merchandise with the indigenous people, and adopted their ideas for trade. The English language originally were surprised to run across that people did not automatically follow the trading customs of England. As more and more colonists came to America, the ethnic people lost some of their power. They began to stockpile goods that they knew the colonists would want to go along their power in the trade. Equally colonists expanded into new spaces, the power dynamic got worse for the indigenous people.[15] The colonists began to exploit the differences between the groups of how important certain goods were. They created debt around the idea of purchasing state. William Pynchon, a settler in what is currently Connecticut, used wampum to gain an advantage in the fur trade. He gave out credit to settlers who helped him create wampum. Later a while of the settlers being in the U.s., land became its ain kind of money. This assisted the colonists in taking the land from the ethnic people.[15]

Canada

In Canada, the Canada Mortgage and Housing Corporation (CMHC) is the country's national housing agency, providing mortgage loan insurance, mortgage-backed securities, housing policy and programs, and housing research to Canadians.[16] It was created past the federal government in 1946 to address the country's postal service-war housing shortage, and to help Canadians achieve their homeownership goals.

The nigh common mortgage in Canada is the v-year fixed-rate closed mortgage, as opposed to the U.Due south. where the near common blazon is the 30-twelvemonth fixed-rate open mortgage.[17] Throughout the financial crisis and the ensuing recession, Canada's mortgage market continued to function well, partly due to the residential mortgage market place'due south policy framework, which includes an effective regulatory and supervisory regime that applies to virtually lenders. Since the crisis, however, the low interest rate surround that has arisen has contributed to a meaning increase in mortgage debt in the country.[18]

In April 2014, the Function of the Superintendent of Financial Institutions (OSFI) released guidelines for mortgage insurance providers aimed at tightening standards effectually underwriting and take chances direction. In a statement, the OSFI has stated that the guideline will "provide clarity about all-time practices in respect of residential mortgage insurance underwriting, which contribute to a stable financial arrangement." This comes after several years of federal government scrutiny over the CMHC, with former Finance Minister Jim Flaherty musing publicly as far dorsum as 2022 about privatizing the Crown corporation.[19]

In an attempt to absurd downward the existent estate prices in Canada, Ottawa introduced a mortgage stress test effective 17 October 2016.[twenty] Under the stress test, every home buyer who wants to go a mortgage from any federally regulated lender should undergo a test in which the borrower's affordability is judged based on a rate that is not lower than a stress charge per unit fix past the Banking concern of Canada. For high-ratio mortgage (loan to value of more than than eighty%), which is insured by Canada Mortgage and Housing Corporation, the rate is the maximum of the stress test rate and the current target rate. However, for uninsured mortgage, the charge per unit is the maximum of the stress test rate and the target interest rate plus 2%. [21] This stress test has lowered the maximum mortgage approved corporeality for all borrowers in Canada.

The stress-test rate consistently increased until its elevation of 5.34% in May 2022 and it was not inverse until July 2022 in which for the first fourth dimension in three years it decreased to five.19%.[22] This decision may reflect the push-back from the existent-manor industry[23] as well as the introduction of the commencement-time home buyer incentive program (FTHBI) by the Canadian authorities in the 2022 Canadian federal budget. Because of all the criticisms from existent manor industry, Canada finance minister Bill Morneau ordered to review and consider changes to the mortgage stress exam in December 2019.[24]

United Kingdom

The mortgage manufacture of the Uk has traditionally been dominated by building societies, but from the 1970s the share of the new mortgage loans market place held by edifice societies has declined essentially. Betwixt 1977 and 1987, the share vicious from 96% to 66% while that of banks and other institutions rose from 3% to 36%. In that location are currently over 200 pregnant separate fiscal organizations supplying mortgage loans to firm buyers in Britain. The major lenders include building societies, banks, specialized mortgage corporations, insurance companies, and alimony funds.

In the UK variable-charge per unit mortgages are more mutual than in the United States.[25] [26] This is in part because mortgage loan financing relies less on fixed income securitized assets (such every bit mortgage-backed securities) than in the United States, Denmark, and Germany, and more on retail savings deposits like Commonwealth of australia and Spain.[25] [26] Thus, lenders adopt variable-rate mortgages to stock-still rate ones and whole-of-term fixed charge per unit mortgages are generally not bachelor. All the same, in recent years fixing the rate of the mortgage for curt periods has become popular and the initial two, 3, five and, occasionally, ten years of a mortgage can be fixed.[27] From 2007 to the beginning of 2022 between 50% and 83% of new mortgages had initial periods fixed in this way.[28]

Home ownership rates are comparable to the The states, just overall default rates are lower.[25] Prepayment penalties during a stock-still charge per unit period are common, whilst the United States has discouraged their use.[25] Similar other European countries and the rest of the world, merely unlike most of the U.s.a., mortgages loans are usually not nonrecourse debt, meaning debtors are liable for any loan deficiencies after foreclosure.[25] [29]

The customer-facing aspects of the residential mortgage sector are regulated by the Financial Conduct Authority (FCA), and lenders' financial probity is overseen by a separate regulator, the Prudential Regulation Authorization (PRA) which is part of the Bank of England. The FCA and PRA were established in 2022 with the aim of responding to criticism of regulatory failings highlighted by the financial crunch of 2007–2008 and its aftermath.[30] [31] [32]

Continental Europe

In most of Western Europe (except Kingdom of denmark, kingdom of the netherlands and Germany), variable-charge per unit mortgages are more common, dissimilar the fixed-charge per unit mortgage common in the United States.[25] [26] Much of Europe has home ownership rates comparable to the United States, only overall default rates are lower in Europe than in the U.s.a..[25] Mortgage loan financing relies less on securitizing mortgages and more on formal government guarantees backed past covered bonds (such every bit the Pfandbriefe) and deposits, except Denmark and Frg where asset-backed securities are likewise common.[25] [26] Prepayment penalties are all the same mutual, whilst the United States has discouraged their use.[25] Different much of the United States, mortgage loans are unremarkably non nonrecourse debt.[25]

Within the European Union, covered bonds market book (covered bonds outstanding) amounted to virtually EUR 2 trillion at year-cease 2007 with Germany, Denmark, Spain, and France each having outstandings above 200,000 EUR million.[33] Pfandbrief-similar securities accept been introduced in more 25 European countries—and in recent years also in the U.S. and other countries outside Europe—each with their own unique law and regulations.[34]

Recent trends

Mortgage rates historical trends 1986 to 2010

On July 28, 2008, U.s.a. Treasury Secretary Henry Paulson announced that, along with 4 big U.S. banks, the Treasury would attempt to kick start a market place for these securities in the United States, primarily to provide an alternative form of mortgage-backed securities.[35] Similarly, in the UK "the Government is inviting views on options for a UK framework to evangelize more affordable long-term fixed-rate mortgages, including the lessons to exist learned from international markets and institutions".[36]

George Soros's Oct 10, 2008 The Wall Street Journal editorial promoted the Danish mortgage market place model.[37]

Malaysia

Mortgages in Malaysia can exist categorised into 2 unlike groups: conventional home loan and Islamic domicile loan. Under the conventional domicile loan, banks commonly charge a fixed interest rate, a variable interest rate, or both. These interest rates are tied to a base of operations rate (individual bank's benchmark rate).

For Islamic home financing, it follows the Sharia Law and comes in 2 mutual types: Bai' Bithaman Ajil (BBA) or Musharakah Mutanaqisah (MM). Bai' Bithaman Ajil is when the bank buys the property at current market price and sells information technology dorsum to yous at a much higher toll. Musharakah Mutanaqisah is when the depository financial institution buys the property together with you. You will then slowly buy the banking concern's portion of the property through rental (whereby a portion of the rental goes to paying for the purchase of a office of the bank's share in the property until the belongings comes to your consummate ownership).

Islamic countries

Islamic Sharia law prohibits the payment or receipt of involvement, meaning that Muslims cannot use conventional mortgages. Yet, real estate is far too expensive for almost people to buy outright using cash: Islamic mortgages solve this problem by having the property change hands twice. In i variation, the bank will buy the house outright and so act as a landlord. The homebuyer, in addition to paying hire, will pay a contribution towards the buy of the property. When the last payment is fabricated, the property changes hands.[ clarification needed ]

Typically, this may atomic number 82 to a higher final price for the buyers. This is considering in some countries (such as the U.k. and India) there is a stamp duty which is a tax charged past the government on a change of ownership. Because buying changes twice in an Islamic mortgage, a postage stamp taxation may exist charged twice. Many other jurisdictions accept like transaction taxes on change of ownership which may exist levied. In the United Kingdom, the dual application of stamp duty in such transactions was removed in the Finance Act 2003 in order to facilitate Islamic mortgages.[38]

An alternative scheme involves the bank reselling the property according to an installment programme, at a price higher than the original price.

Both of these methods compensate the lender every bit if they were charging interest, merely the loans are structured in a way that in proper noun they are not, and the lender shares the fiscal risks involved in the transaction with the homebuyer.[ citation needed ]

Mortgage insurance

Mortgage insurance is an insurance policy designed to protect the mortgagee (lender) from any default by the mortgagor (borrower). It is used commonly in loans with a loan-to-value ratio over 80%, and employed in the event of foreclosure and repossession.

This policy is typically paid for by the borrower as a component to last nominal (note) rate, or in one lump sum upwards front, or equally a separate and itemized component of monthly mortgage payment. In the last case, mortgage insurance can be dropped when the lender informs the borrower, or its subsequent assigns, that the property has appreciated, the loan has been paid down, or whatsoever combination of both to relegate the loan-to-value under 80%.

In the event of repossession, banks, investors, etc. must resort to selling the property to recoup their original investment (the money lent) and are able to dispose of hard avails (such as existent estate) more quickly by reductions in price. Therefore, the mortgage insurance acts as a hedge should the repossessing authority recover less than full and fair market place value for whatsoever hard asset.

See also

- Commercial mortgage

- Mortgage analytics

- No Income No Nugget (NINA)

- Nonrecourse debt

- Refinancing

- Second Mortgage

- Buy to permit

- Mortgage cashback

- Remortgage

- UK mortgage terminology

- Commercial lender (US) – a term for a lender collateralizing non-residential properties.

- eMortgages

- FHA loan – Relating to the U.S. Federal Housing Administration

- Fixed charge per unit mortgage calculations (USA)

- Location Efficient Mortgage – a type of mortgage for urban areas

- Mortgage assumption

- pre-blessing – U.South. mortgage terminology

- pre-qualification – U.South. mortgage terminology

- Predatory mortgage lending

- VA loan – Relating to the U.Southward. Department of Veterans Diplomacy.

Other nations

- Danish mortgage market

- Hypothec - equivalent in civil law countries

- Mortgage Investment Corporation

Legal details

- Human activity – legal aspects

- Mechanics lien – a legal concept

- Perfection – applicative legal filing requirements

References

- ^ Coke, Edward. Commentaries on the Laws of England.

[I]f he doth not pay, then the Land which is put in pledge upon condition for the payment of the coin, is taken from him for always, and so dead to him upon condition, &c. And if he doth pay the coin, then the pledge is dead as to the Tenant

- ^ FTC. Mortgage Servicing: Making Certain Your Payments Count.

- ^ "How Long Does Mortgage Underwriting Take?". homeguides.sfgate.com. SFGate. Retrieved 9 December 2016.

- ^ "What Is an Underwriter: The Unseen Approver of Your Mortgage". 26 Feb 2014.

- ^ "Who Needs Mortgage Loan Insurance?". Canadian Mortgage and Housing Corporation. Retrieved 2009-01-thirty .

- ^ Bodine, Alicia (Apr 5, 2019). "Definition of Mortgage Curtailment". budgeting.thenest.com. Certified Ramsey Solutions Principal Financial Motorcoach (Updated).

- ^ "How practice HECM Reverse Mortgages Work?". The Mortgage Professor.

- ^ Are Mortgage Assumptions a Adept Deal?. Mortgage Professor.

- ^ Cortesi GR. (2003). Mastering Real Estate Principals. p. 371

- ^ Homes: Slow-marketplace savings – the 'buy-down'. CNN Money.

- ^ http://world wide web.unece.org/hlm/prgm/hmm/hsg_finance/publications/housing.finance.system.pdf , p. 46

- ^ Renuart Due east. (2012). Property Title Trouble in Not-Judicial Foreclosure States: The Ibanez Fourth dimension Bomb?. Albany Constabulary School

- ^ Unmarried-family unit notes. Fannie Mae.

- ^ Security Instruments. Fannie Mae.

- ^ a b c d Park, Sue (2016). "Money, Mortgages, and the Conquest of America". Constabulary & Social Inquiry. 41 (4): 1006–1035. doi:10.1111/lsi.12222. S2CID 157705999.

- ^ "Near CMHC - CMHC". CMHC.

- ^ "Comparing Canada and U.S. Housing Finance Systems - CMHC". CMHC.

- ^ Crawford, Allan. "The Residential Mortgage Market place in Canada: A Primer" (PDF). bankofcanada.ca.

- ^ Greenwood, John (14 April 2014). "New mortgage guidelines push button CMHC to cover insurance nuts". Financial Mail.

- ^ "New mortgage stress exam rules kick in today". CBC News. Retrieved eighteen March 2019.

- ^ "Mortgage Qualifier Tool". Government of Canada. xi May 2012.

- ^ Evans, Pete (July 19, 2019). "Mortgage stress exam rules get more lenient for beginning time". CBC News . Retrieved October thirty, 2019.

- ^ Zochodne, Geoff (June 11, 2019). "Regulator defends mortgage stress test in face of push-back from industry". Financial Mail service . Retrieved October 30, 2019.

- ^ Zochodne, Geoff (13 Dec 2019). "Finance government minister Bill Morneau to review and consider changes to mortgage stress exam". Fiscal Mail service.

- ^ a b c d e f one thousand h i j Congressional Budget Office (2010). Fannie Mae, Freddie Mac, and the Federal Role in the Secondary Mortgage Market place. p. 49.

- ^ a b c d International Budgetary Fund (2004). Earth Economic Outlook: September 2004: The Global Demographic Transition. pp. 81–83. ISBN978-one-58906-406-five.

- ^ "All-time fixed rate mortgages: 2, three, v and 10 years". The Telegraph. 26 February 2014. Archived from the original on 2022-01-11. Retrieved 10 May 2014.

- ^ "Demand for fixed mortgages hits all-fourth dimension high". The Telegraph. 17 May 2013. Archived from the original on 2022-01-11. Retrieved 10 May 2014.

- ^ United Nations (2009). Forest Products Annual Market Review 2008-2009. Un Publications. p. 42. ISBN978-92-i-117007-eight.

- ^ Vina, Gonzalo. "U.M. Scraps FSA in Biggest Bank Regulation Overhaul Since 1997". Businessweek. Bloomberg L.P. Retrieved 10 May 2014.

- ^ "Regulatory Reform Background". FSA web site. FSA. Retrieved 10 May 2014.

- ^ "Fiscal Services Bill receives Purple Assent". HM Treasury. 19 December 2012. Retrieved ten May 2014.

- ^ "Covered Bail Outstanding 2007".

- ^ "UNECE Homepage" (PDF). www.unece.org.

- ^ owner, proper noun of the document. "FDIC: Printing Releases - PR-60-2008 7/15/2008". www.fdic.gov.

- ^ "Housing Finance Review: assay and proposals. HM Treasury, March 2008" (PDF).

- ^ Soros, George (10 October 2008). "Denmark Offers a Model Mortgage Marketplace". Wall Street Journal – via www.wsj.com.

- ^ "SDLTM28400 - Stamp Duty State Revenue enhancement Transmission - HMRC internal manual - GOV.UK". world wide web.hmrc.gov.united kingdom.

External links

- Mortgages at Curlie

- Mortgages: For Home Buyers and Homeowners at U.s.a..gov

- Australian Securities & Investments Commission (ASIC) Dwelling house Loans

Source: https://en.wikipedia.org/wiki/Mortgage_loan

0 Response to "Can You Get a Mortgage for a Mobile Home"

Post a Comment